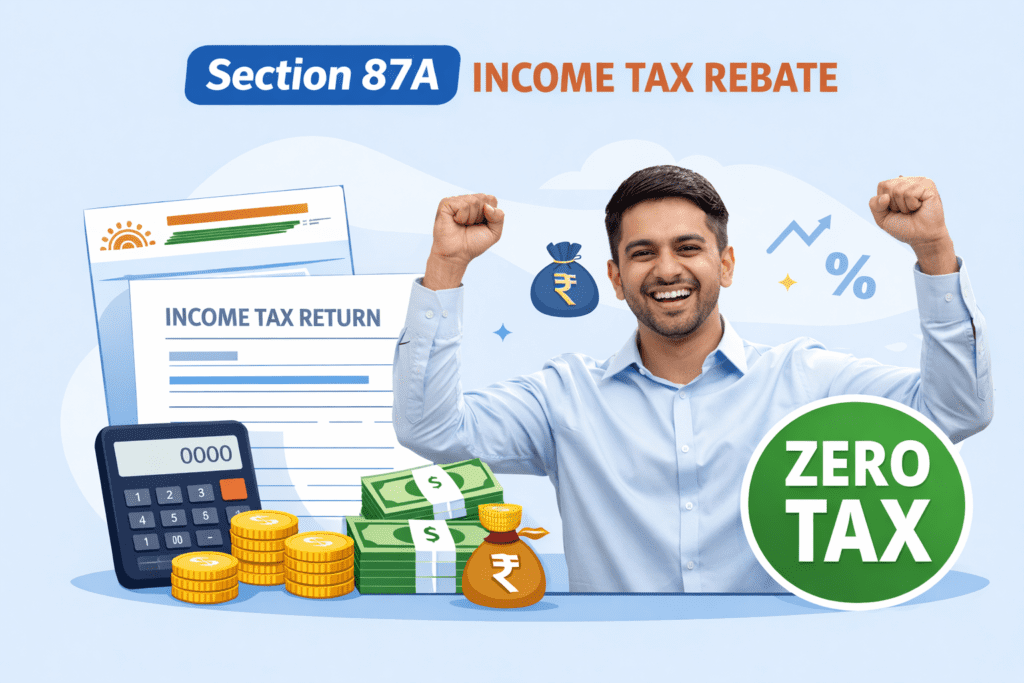

Income Tax Rebate u/s 87A FY 2025-26 (AY 2026-27) को और अधिक प्रभावी बनाकर सरकार ने मध्यम और कम आय वर्ग के टैक्सपेयर्स को बड़ी राहत दी है।

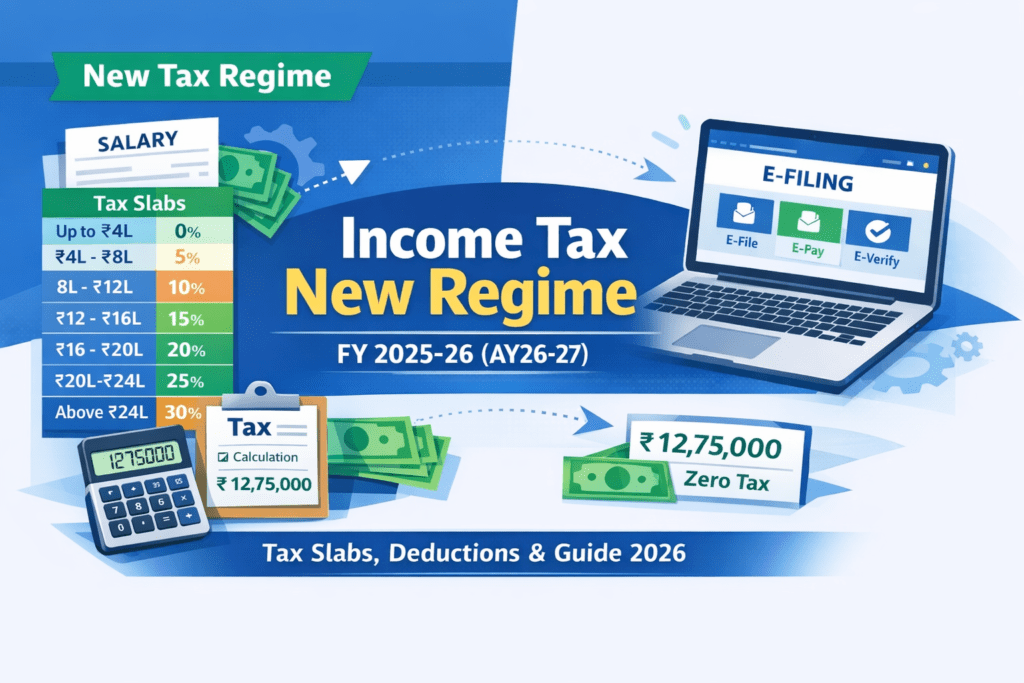

New Tax Regime के तहत अब ₹12 लाख तक की taxable income पर ₹60,000 तक की rebate उपलब्ध है, जिससे eligible taxpayers की पूरी income tax liability zero हो सकती है।

इस article में आप जानेंगे:

- Income Tax Rebate u/s 87A FY 2025-26 क्या है और यह कैसे काम करती है

- New vs Old Tax Regime में Section 87A का अंतर

- Marginal Relief कैसे लागू होती है (examples के साथ)

- Practical tax calculation examples

- ITR में rebate claim करने का आसान और सही तरीका

What is Income Tax Rebate u/s 87A FY 2025-26?

Rebate u/s 87A आयकर अधिनियम, 1961 का एक महत्वपूर्ण प्रावधान है, जिसके तहत सरकार मध्यम और कम आय वाले resident individuals को income tax में सीधी राहत प्रदान करती है। यह rebate किसी deduction की तरह taxable income से नहीं घटती, बल्कि calculate किए गए income tax से सीधे कम की जाती है।

इसका उद्देश्य उन करदाताओं की tax liability को कम करना या पूरी तरह समाप्त करना है, जिनकी आय सरकार द्वारा निर्धारित सीमा के भीतर आती है।

यह rebate Health & Education Cess जोड़ने से पहले लागू होती है, जिससे eligible taxpayers को वास्तविक टैक्स बचत का लाभ मिलता है और कई मामलों में उन्हें कोई income tax नहीं देना पड़ता।

Rebate u/s 87A का इतिहास (FY-wise Timeline)

Rebate u/s 87A को समय-समय पर सरकार द्वारा अपडेट किया गया है।

नीचे दिए गए FY-wise timeline में Section 87A से जुड़े बदलावों, जिससे यह समझना आसान हो जाता है कि अलग-अलग वित्तीय वर्षों में taxpayers को कितना लाभ मिला है।

| Financial Year (FY) | Details |

| FY 2013-14 | Section 87A को पहली बार Income Tax Act में शामिल किया गया। उद्देश्य कम आय वाले resident individuals को income tax से राहत देना था। |

| FY 2014-15 से FY 2018-19 | Rebate की income limit और rebate amount सीमित रही, लेकिन lower income group को basic tax relief मिलती रही। |

| FY 2019-20 | Rebate की income limit बढ़ाकर ₹5 लाख कर दी गई और अधिकतम rebate ₹12,500 तय की गई, जिससे ₹5 लाख तक की income पूरी तरह tax-free हो गई। |

| FY 2020-21 | New Tax Regime की शुरुआत हुई, हालांकि Section 87A की rebate limits में कोई बदलाव नहीं किया गया। |

| FY 2023-24 & 24-25 | New Tax Regime को Default Regime घोषित किया गया। Rebate limit बढ़ाकर ₹7 लाख कर दी गई, जिससे New Regime अधिक attractive बनी। |

| FY 2025-26 | Section 87A में अब तक का सबसे बड़ा बदलाव किया गया। New Tax Regime के तहत income limit बढ़ाकर ₹12 लाख और maximum rebate ₹60,000 कर दी गई। |

Income Tax Rebate u/s 87A FY 2025-26 Limits (New & Old Regime)

नीचे दिए गए table से आप आसानी से समझ सकते हैं कि New और Old Tax Regime में Section 87A की rebate limits क्या हैं:

New Tax Regime

| Particular | Details |

| Income Limit | ₹12,00,000 |

| Maximum Rebate | ₹60,000 |

| Result | ₹12 लाख तक Zero Tax |

Old Tax Regime

| Particular | Details |

| Income Limit | ₹5,00,000 |

| Maximum Rebate | ₹12,500 |

| Result | ₹5 लाख तक Zero Tax |

Rebate U/S 87A – Eligibility Criteria

नीचे दिए गए points से आप समझ पाएँगे कि Section 87A rebate किन taxpayers को मिलती है और किन conditions पर मिलती है।

Resident Individual Eligibility

- यह rebate केवल resident individual taxpayers को उपलब्ध है।

- Non-resident individuals, HUF, companies, firms या LLPs इस rebate के लिए eligible नहीं हैं।

Income Limit Criteria

- New Tax Regime: कुल taxable income ₹12 लाख तक हो।

- Old Tax Regime: कुल taxable income ₹5 लाख तक हो।

- यदि आपकी income इन limits से अधिक है, तो आप केवल Marginal Relief के लिए qualify कर सकते हैं, लेकिन पूरा rebate नहीं मिलेगा।

Rebate Limited to Tax Liability

- Section 87A के तहत मिलने वाली rebate हमेशा tax payable (before cess) तक ही सीमित होती है।

- इसका मतलब यह है कि यदि आपका calculated tax rebate से कम है, तो केवल उतना ही rebate मिलेगा।

Rebate Not Available on LTCG & STCG (111A / 112A)

- Section 87A की rebate Long-Term Capital Gains (LTCG) under Section 112A और Short-Term Capital Gains (STCG) under Section 111A पर नहीं लागू होती।

- यह केवल normal slab rate taxable income पर ही लागू होती है।

Automatic Rebate Calculation in ITR

- यदि आपकी total income ऊपर बताई गई limits के भीतर है, तो ITR भरते समय rebate portal द्वारा automatically calculate हो जाती है।

- आपको अलग से apply करने की जरूरत नहीं होती।

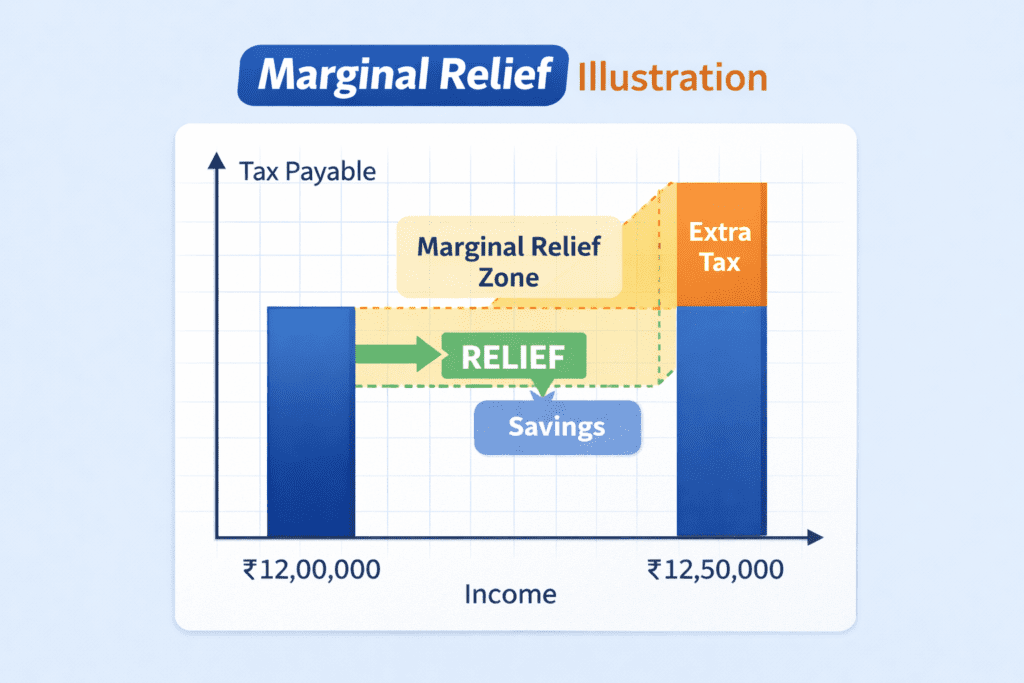

Marginal Relief under Section 87A – Explained with Examples

Marginal Relief उन taxpayers के लिए लागू होता है जिनकी income New Tax Regime में ₹12 लाख के ऊपर थोड़ी अधिक होती है। इसका उद्देश्य यह है कि additional income पर लगाया गया tax, उनकी वास्तविक अतिरिक्त आय से ज्यादा न हो।

When Does Marginal Relief Apply? (कब लागू होता है)

- जब कोई taxpayer की total taxable income ₹12 लाख से थोड़ा अधिक हो।

- और calculated tax इस अतिरिक्त income से ज्यादा हो जाए।

How Marginal Relief Works? (कैसे काम करता है)

- इस स्थिति में taxpayer को केवल ₹12 लाख से ऊपर की अतिरिक्त आय पर tax देना होगा।

- यानी यदि extra tax अधिक है तो marginal relief के तहत tax liability कम कर दी जाती है, ताकि taxpayer को ज्यादा tax न देना पड़े।

Marginal Relief Calculation Steps

| Step & Description | Formula / Calculation |

|---|---|

| Step 1: Excess income above ₹12 lakh निकालें – Total Income में से ₹12,00,000 घटाएँ। | Excess Income (A) = Total Income – ₹12,00,000 |

| Step 2: Total Income पर tax calculate करें (Before Cess)। | Tax on Total Income (B) |

| Step 3: यदि B > A, तो Rebate u/s 87A calculate करें। | Rebate u/s 87A = B – A |

| Step 4: Tax Payable निकालें। | Tax Payable = Total Tax – Rebate + Health & Education Cess |

Marginal Relief Example (FY 2025-26)

इस उदाहरण से आप आसानी से समझ सकते हैं कि Marginal Relief कैसे लागू होता है।

| Example | Total Income (₹) | Excess above ₹12 Lakh (A) | Tax on Total Income (B) | Maximum Rebate u/s 87A (B – A) | Tax Payable + 4% Cess |

| (1) | (2) | (3) {1*Slab NR} | (4) {3-2} | (5) {3-4}+4% | |

| 1 | 12,05,000 | 5,000 | 25,250 | 20,250 | 5,000 + 4% Cess = 5,200 |

| 2 | 12,10,000 | 10,000 | 50,500 | 40,500 | 10,000 + 4% Cess = 10,400 |

| 3 | 12,15,000 | 15,000 | 62,250 | 47,250 | 15,000 + 4% Cess = 15,600 |

| 4 | 12,20,000 | 20,000 | 65,000 | 45,000 | 20,000 + 4% Cess = 20,800 |

| 5 | 12,25,000 | 25,000 | 68,750 | 43,750 | 25,000 + 4% Cess = 26,000 |

| 6 | 12,30,000 | 30,000 | 72,500 | 42,500 | 30,000 + 4% Cess = 31,200 |

| 7 | 12,40,000 | 40,000 | 80,500 | 40,500 | 40,000 + 4% Cess = 41,600 |

| 8 | 12,50,000 | 50,000 | 1,02,500 | 52,500 | 50,000 + 4% Cess = 52,000 |

| 9 | 12,60,000 | 60,000 | 1,05,500 | 45,500 | 60,000 + 4% Cess = 62,400 |

| 10 | 12,75,000 | 75,000 | 1,12,500 | 37,500 | 75,000 + 4% Cess = 78,000 |

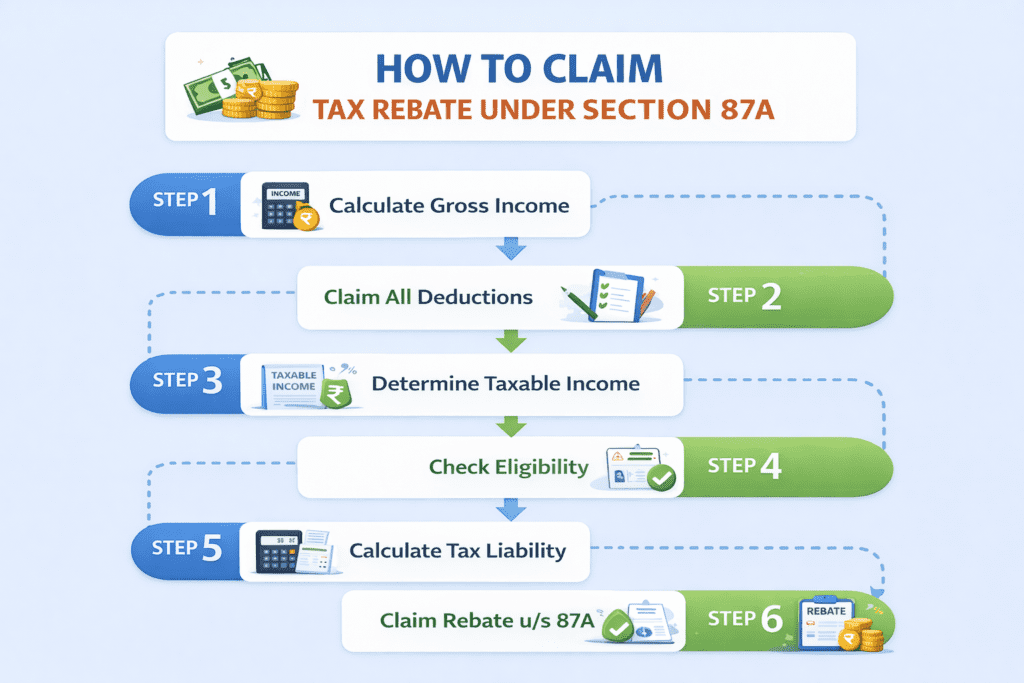

How to Claim Section 87A Rebate in ITR (Step-by-Step)

Section 87A के तहत rebate claim करना बहुत आसान है। यदि आपकी income New Tax Regime में ₹12 लाख या Old Tax Regime में ₹5 लाख तक है, तो यह rebate ITR में अपने आप लागू हो जाती है।

नीचे दिए गए step-by-step guide में आप आसानी से समझ सकते हैं कि Section 87A rebate कैसे claim करें और tax filing में इसका पूरा लाभ कैसे उठाएँ।

| Step | Details |

| Step 1: Gross Total Income Calculate करें | अपने salary, business income, capital gains और अन्य sources को जोड़कर FY 2025-26 का gross total income निकालें। |

| Step 2: Tax Deductions घटाएँ | Old Tax Regime में applicable deductions (जैसे Section 80C, 80D, 80CCD, 80G) घटाएँ। New Tax Regime में अधिकांश deductions नहीं मिलते। |

| Step 3: Total Taxable Income निकालें | Step 1 और Step 2 के बाद आपकी total taxable income निकल जाएगी। |

| Step 4: ITR में Declare करें | अपनी gross income और deductions को ITR फॉर्म में सही ढंग से declare करें। New Tax Regime में rebate automatically calculate हो जाती है। |

| Step 5: Rebate Claim करें | Section 87A के तहत rebate को ITR में apply करें। New Tax Regime: ₹12 लाख तक की income पर ₹60,000 तक की rebate। Old Tax Regime: ₹5 लाख तक की income पर ₹12,500 rebate। |

| Step 6: Tax Payment और Refund Check करें | Rebate apply करने के बाद बचा हुआ tax (यदि कोई हो) जमा करें। Excess TDS या advance tax refundable हो सकता है। |

Section 87A Rebate Example – New Tax Regime

| Example | Total Income (₹) | Tax on Total Income (Before Cess) | Rebate u/s 87A | Tax Payable + 4% Cess |

| 1 | 4,00,000 | 0 | 0 | 0 + 4% Cess = 0 |

| 2 | 5,00,000 | 5,000 | 5,000 | 0 + 4% Cess = 0 |

| 3 | 6,50,000 | 32,500 | 32,500 | 0 + 4% Cess = 0 |

| 4 | 12,00,000 | 60,000 | 60,000 | 0 + 4% Cess = 0 |

Section 87A Rebate Example – Old Tax Regime

| Example | Gross Income (₹) | Deduction u/s 80C (₹) | Total Income (₹) | Income Tax (₹) | Rebate u/s 87A (₹) | Tax Payable (₹) |

| 1 | 4,50,000 | 50,000 | 4,00,000 | 0 | 0 | Nil |

| 2 | 5,50,000 | 50,000 | 5,00,000 | 12,500 | 12,500 | Nil |

Rebate Against Various Tax Liabilities

Section 87A की rebate सिर्फ normal slab rate से taxable income पर लागू होती है। Special rate से taxable income पर इस rebate का लाभ नहीं मिलता।

Eligible Income for Section 87A Rebate

- Salary, pension, business income और अन्य normal slab rate वाली income

- Long-Term Capital Gains (LTCG) under Section 112 (जिनपर normal slab rate लागू होता है)

Example:

- Salary: ₹10,00,000 – Eligible

- LTCG under Sec 112: ₹2,00,000 – Eligible

Ineligible Income for Section 87A Rebate

- Equity shares और equity-oriented mutual funds पर होने वाला LTCG under Section 112A (10%)

- Listed equity shares एवं equity-oriented mutual funds पर STCG under Section 111A (15%)

- Lottery, betting, gambling आदि की income (Section 115BB)

Example:

- LTCG on Equity shares: ₹1,50,000 – Not Eligible

- STCG on Mutual Funds: ₹50,000 – Not Eligible

- Lottery winning: ₹1,00,000 – Not Eligible

FAQs – Income Tax Rebate u/s 87A FY 2025-26

Income Tax Rebate u/s 87A FY 2025-26 क्या है?

Section 87A के तहत eligible resident taxpayers को उनकी income पर tax rebate मिलता है। FY 2025-26 में New Tax Regime में ₹12 लाख तक की income पर ₹60,000 तक और Old Tax Regime में ₹5 लाख तक की income पर ₹12,500 तक rebate मिलती है।

Rebate claim करने के लिए eligibility क्या है?

केवल resident individuals जो New Tax Regime में ₹12 लाख तक या Old Tax Regime में ₹5 लाख तक की taxable income रखते हैं, rebate claim कर सकते हैं।

Income Tax Rebate u/s 87A FY 2025-26 कितनी मिलती है?

New Tax Regime: ₹12 लाख तक की income पर ₹60,000 तक

Old Tax Regime: ₹5 लाख तक की income पर ₹12,500 तक

Marginal Relief क्या है?

यदि आपकी income New Tax Regime में ₹12 लाख से थोड़ी अधिक है और extra tax ज्यादा बन रहा है, तो Marginal Relief की वजह से excess income परही tax देना होता है, जिससे taxpayers को राहत मिलती है।

Rebate claim करने का तरीका क्या है?

ITR फाइल करते समय आपकी gross income और deductions सही ढंग से declare करें। यदि आप eligible हैं, तो rebate automatically ITR में calculate हो जाती है।

क्या rebate New और Old दोनों Regime में अलग-अलग है?

हाँ। New Tax Regime में limit ₹12 लाख और rebate ₹60,000 है, जबकि Old Tax Regime में limit ₹5 लाख और rebate ₹12,500 है।

Income Tax Rebate u/s 87A FY 2025-26 – Quick Summary

- Eligibility: केवल Resident Individual Taxpayers के लिए।

- New Tax Regime: Income up to ₹12,00,000 – Maximum Rebate ₹60,000

- Old Tax Regime: Income up to ₹5,00,000 – Maximum Rebate ₹12,500

- Rebate calculation: Income tax से घटाई जाती है (Health & Education Cess लगाने से पहले)

- Marginal Relief: यदि आपकी taxable income ₹12,00,001 या उससे थोड़ी अधिक है, तो Marginal Relief की सुविधा मिलती है, ताकि sudden tax jump न हो।

- ITR Filing: Rebate automatically calculate हो जाती है ITR software में।

निष्कर्ष (Conclusion) – Section 87A Rebate (FY 2025-26)

Section 87A rebate मध्यम और कम आय वर्ग के taxpayers के लिए एक बड़ा राहत पैकेज है।

- New Tax Regime: ₹12 लाख तक की income पर ₹60,000 तक की rebate, जिससे eligible taxpayers की tax liability पूरी तरह समाप्त हो सकती है।

- Old Tax Regime: ₹5 लाख तक की income पर rebate, जिससे low-income taxpayers को फायदा मिलता है।

- Claiming Rebate: ITR में rebate automatically calculate होती है, और Marginal Relief थोड़ी अधिक income पर भी अतिरिक्त tax से बचाव देती है।

Tax planning के लिए Section 87A rebate को ignore न करें। सही regime चुनकर और ITR सही तरीके से file करके आप legally zero tax का फायदा उठा सकते हैं। Tax calculator से अपनी exact tax liability जरूर check करें।

सारांश: Section 87A rebate का सही उपयोग करके आप अपने टैक्स बोझ को कम कर सकते हैं और ज्यादा बचत कर सकते हैं। इसे अपनी tax planning में जरूर शामिल करें।